Artificial intelligence (AI) and automation technologies are transforming service industries, including finance, healthcare, hospitality, retail, education, public services and digital platforms. While algorithmic decision-making systems, service robots, chatbots, predictive analytics and automated workflows offer enhanced efficiencies, personalization possibilities and scalability potential, these technologies are also raising profound ethical concerns related to their modus operandi and explainability of their outputs (Camilleri, 2024; Hu & Min, 2023).

As AI-driven service systems increasingly mediate interactions between organisations and their stakeholders; ethical failures and bias have the potential to reinforce existing social inequalities, undermine their trustworthiness, service quality, organisational legitimacy and broader societal well-being (Camilleri et al., 2024). Moreover, opaque “black-box” models reduce transparency and could erode user trust in these machine learning technologies (Kordzadeh & Ghasemaghaei, 2022). Unclear accountability structures may obscure responsibility for service failures or might facilitate unintended harmful outcomes (Novelli et al., 2024). These challenges are particularly evidenced in service contexts where human–AI interactions are frequent, relational and consequential.

Such concerns are clearly illustrated in healthcare services (Procter et al., 2023), where AI-driven diagnostic and triage systems are increasingly used to support clinical decision-making. When these technologies rely on biased or unrepresentative training data, they may systematically underdiagnose or misclassify specific demographic groups. Given the high-stakes and the relational nature of healthcare encounters, limited transparency and explainability can significantly diminish patient trust while raising serious ethical and accountability concerns.

Similar issues arise in financial and insurance services (Oke & Cavus, 2025), where automated credit scoring, loan approval and underwriting systems directly influence individuals’ financial inclusion and long-term economic prospects. Algorithmic opacity makes it difficult for customers to understand, question or contest adverse decisions. Therefore, biased models may perpetuate or amplify socioeconomic inequalities. Such an outcome is particularly problematic in service relationships characterised by long-term dependency and trust.

Ethical challenges are also conspicuous in customer service and frontline interactions (Han et al., 2023), where chatbots and virtual assistants handle large volumes of customer inquiries across retail, telecommunications and travel services (Lv et al., 2022). Although these systems offer efficiency and scalability benefits, there are instances where they fail to recognise emotional distress, cultural differences, or exceptional circumstances. Excessive automation can therefore undermine relational service quality, especially when customers are unable to escalate complex or sensitive issues to human agents (Yang et al., 2022).

In public service contexts, governments are progressively deploying AI systems (Willems et al., 2023) to allocate welfare benefits, determine assess eligibility and detect fraud. In such settings, automated decisions can have profound implications for the citizens’ livelihoods and their inclusion in cohesive societies Ethical concerns become particularly acute when accountability is diffused between public agencies and technology providers, as well as when affected individuals lack meaningful mechanisms for appeal, explanation or redress.

Likewise, platform-based and gig economy services are increasingly relying on algorithmic management systems to assign tasks, evaluate performance and to compute remunerations (Kadolkar et al., 2025). These systems often operate as “black boxes,” leaving workers uncertain about how ratings, penalties or income calculations are determined. The resulting lack of transparency and of clear accountability structures can weaken trust, exacerbate power asymmetries and could intensify worker vulnerability within ongoing service relationships.

Notwithstanding, more human resource management and recruitment specialists are adopting AI-enabled tools for résumé screening and to assess their candidates’ credentials (Soleimani et al., 2025). Possible bias embedded within these systems may disadvantage certain social groups. Their limited transparency can prevent applicants from understanding how hiring decisions are made. Such practices raise important ethical questions concerning fairness, informed consent and procedural justice within professional service contexts.

This special issue seeks to advance novel insights into the above ethical implications of AI and automation in services industries. The guest editors look forward to receiving original, interdisciplinary contributions that critically examine how ethical principles can be embedded into the design, governance, implementation and evaluation of AI-enabled service systems.

Aims and scope

The special issue aims to:

· Deepen understanding of ethical risks and dilemmas associated with AI and automation in service industries.

· Explore mechanisms for bias detection, mitigation and governance in service algorithms.

· Examine transparency, explainability and accountability in AI-enabled service encounters.

· Advance responsible, human-centered and sustainable approaches to AI-driven service innovation.

Both conceptual, theoretical and empirical contributions are welcome, including qualitative, quantitative, mixed-methods, experimental, design science as well as critical and/or reflexive approaches.

Indicative themes and topics

Submissions may address, but are not limited to, the following topics:

· Algorithmic bias and discrimination in service delivery;

· Ethical design of AI-enabled service systems;

· Transparency and explainability in automated service decisions;

· Accountability and responsibility in human–AI service interactions;

· AI ethics governance, regulation, and standards in service industries;

· Trust, legitimacy and customer perceptions of AI-driven services;

· Ethical implications of service robots and conversational agents;

· Human oversight and hybrid human–AI service models;

· Data privacy, surveillance and consent in digital service platforms;

· Fairness and inclusion in AI-based personalisation and targeting;

· Responsible AI and ESG considerations in service organisations;

· Cross-cultural and institutional perspectives on AI ethics in services;

· Ethical failures, service recovery and crisis communication involving AI;

· Methodological advances for studying ethics in AI-enabled services.

References

Camilleri, M. A., Zhong, L., Rosenbaum, M. S. & Wirtz, J. (2024). Ethical considerations of service organizations in the information age. The Service Industries Journal, 44(9-10), 634-660.

Camilleri, M. A. (2024). Artificial intelligence governance: Ethical considerations and implications for social responsibility. Expert Systems, 41(7), e13406.

Hu, Y., & Min, H. K. (2023). The dark side of artificial intelligence in service: The “watching-eye” effect and privacy concerns. International Journal of Hospitality Management, 110, 103437.

Kadolkar, I., Kepes, S., & Subramony, M. (2025). Algorithmic management in the gig economy: A systematic review and research integration. Journal of Organizational Behavior, 46(7), 1057-1080.

Kordzadeh, N., & Ghasemaghaei, M. (2022). Algorithmic bias: review, synthesis, and future research directions. European Journal of Information Systems, 31(3), 388-409.

Lv, X., Yang, Y., Qin, D., Cao, X., & Xu, H. (2022). Artificial intelligence service recovery: The role of empathic response in hospitality customers’ continuous usage intention. Computers in Human Behavior, 126, 106993.

Novelli, C., Taddeo, M., & Floridi, L. (2024). Accountability in artificial intelligence: What it is and how it works. AI & Society, 39(4), 1871-1882.

Procter, R., Tolmie, P., & Rouncefield, M. (2023). Holding AI to account: challenges for the delivery of trustworthy AI in healthcare. ACM Transactions on Computer-Human Interaction, 30(2), 1-34.

Soleimani, M., Intezari, A., Arrowsmith, J., Pauleen, D. J., & Taskin, N. (2025). Reducing AI bias in recruitment and selection: an integrative grounded approach. The International Journal of Human Resource Management, 1-36.

Willems, J., Schmid, M. J., Vanderelst, D., Vogel, D., & Ebinger, F. (2023). AI-driven public services and the privacy paradox: do citizens really care about their privacy?. Public Management Review, 25(11), 2116-2134.

Yang, Y., Liu, Y., Lv, X., Ai, J., & Li, Y. (2022). Anthropomorphism and customers’ willingness to use artificial intelligence service agents. Journal of Hospitality Marketing & Management, 31(1), 1-23.

Submission Instructions

Submission guidelines

Manuscripts should be prepared according to The Service Industries Journal’s author guidelines and submitted via the journal’s online submission system. During submission, authors should select the special issue title:

“Ethical implications of artificial intelligence (AI) and automation in service industries: Addressing algorithmic bias, opacity and unclear accountability mechanisms”.

All submissions will undergo a double-blind peer review process in accordance with the journal’s standards and policies of Taylor & Francis.

Important dates

Full paper submission deadline: 31st January 2027

First round of reviews: 31st March 2027

Revised manuscript submission: 31st May 2027

Final acceptance: 31st August 2027

Expected publication: 30th November 2027

Contact Information: For informal enquiries regarding the fit of manuscripts or the scope of the special issue, please contact the Leading Guest Editor via Mark.A.Camilleri@um.edu.mt.

I have just returned back to base after a productive two-day foreign expert meeting.

Once again, it was a positive experience to connect with European academic colleagues, to review and discuss research proposals worth thousands of Euros.

My big congratulations go to the successful scholars who passed the shortlisting phase, based on our evaluation scores.

The best proposals will eventually receive national government funds for transformative projects that will add value to society and the natural environment.

Featuring snippets from an article that was accepted for publication through Springer’s “Service Business”.

Suggested citation: Camilleri, M.A., Bhatnagar, S.B. & Chakraborty, D. (2025). Exaggerated statements in online consumer reviews: Causes and implications. Service Business, 19, Art. 19, https://doi.org/10.1007/s11628-025-00590-6

Abstract

This study investigates the factors that contribute to the creation of inflated consumer testimonials. Quantitative data were gathered from four hundred forty (440) respondents who shared their service experiences through popular social media platforms. A covariance-based structural equations model approach has been used to analyze the data. The results suggest that psychological and emotional factors including the consumers’ self-image, self-enhancement as well as their motivations for retribution against service providers, are having a significant effect on the development of amplified review content.

Researchers have frequently reported that certain individuals tend to misrepresent facts and may willingly decide to deceive other persons, in their daily conversations, including in virtual ones (Moqbel and Jain 2025; Sahut et al. 2024). It is very likely that such persons would fabricate content when they engage in online conversations (Plotkina et al. 2020) and may even create inflated claims in their user generated content, while sharing personal experiences with online users (Belarmino et al. 2022; Bozkurt et al. 2023). Electronic word of mouth communications, like online reviews, are not always truthful (Camilleri, 2022; Kapoor et al. 2021; Lee et al. 2022; Tomazelli et al. 2024), as they may frequently feature inflated claims (Román et al. 2023). A few researchers have even suggested that exaggerated reviews can have an adverse effect on their credibility (Chatterjee et al. 2023).

A lack of credibility and trustworthiness in online reviews could negatively affect the consumers’ perceptions and attitudes toward the business (Camilleri and Filieri 2023; Tan and Chen 2023). For instance, Fong et al. (2024) distinguished between trustworthy and untrustworthy content presented in online consumer testimonials. Yet, for the time being, there is still scarce research focused on the propagation of inflated claims in online reviews (Arif and Chandwani 2024). Various researchers have often attempted to find ways to detect misinformation and prefabricated online content including in social media and review platforms (Chen et al. 2022).

However, in many cases, it proves difficult to recognize the identities of those reviewers who are sharing overblown and deceitful statements about their experiences in online platforms (Bylok 2022). Notwithstanding, there may be different reasons why individuals engage in deceptive behaviors. People may decide to deceive others for personal gain, and/or to protect their own image or reputation. Their intention could be to manipulate others to achieve desired outcomes (Min and Wakslak 2022). Alternatively, they may rationalize their deceitful behaviors due to psychological factors. Such individuals would probably convince themselves that their actions are justified or harmless (Costa Filho et al. 2023; Petrescu et al. 2022).

Undoubtedly, the topic about deceitful, unreliable and inflated online reviews warrants further investigation, as these electronic word-of-mouth communications may constitute false advertising or fraud. Prospective consumers can be manipulated and misled into buying substandard or misrepresented products/services. For example, the use of generative AI could exacerbate the pervasiveness of fake inflated review content with high linguistic sophistication. Hence, it may prove hard for online users to detect the legitimacy and veracity of consumer reviews. Certainly, further investigation is warranted on this topic, to better understand the incidence and the scale of the exaggerated claims featured in user-generated content, their underlying motivations and drivers, as well as the identification of technological and regulatory responses.

In this light, this research identifies the factors and the extent to which online users share overstatements and amplified assertions in consumer review platforms. Specifically, the underlying research questions are: [RQ1] How and to what extent are the consumers’ altruistic intentions to provide customer-focused reviews contributing to the development of exaggerated claims in their testimonials? [RQ2] How and to what extent are the consumers’ constructive reviews aimed at service providers having an effect on the development of exaggerated claims in their testimonials? [RQ3] How and to what extent are the consumers’ psychological factors including their self-esteem and self-image having an effect on the development of exaggerated claims in their testimonials? [RQ4] How and to what extent are the consumers’ dissatisfaction levels with the services they receive and their retribution motivations having an effect on the development of exaggerated claims in their testimonials?

This empirical study builds on extant theoretical underpinnings related to the interpersonal deception theory (Buller and Burgoon 1996; Buller et al. 1996; Burgoon 2015; Gaspar et al. 2022) to delve into the factors that can lead consumers to create inflated claims in online reviews (Hill Cummings et al. 2024; Valdez et al. 2018). The researchers validate constructs that were tried and tested in academia including altruistic motivations to support prospects and/or businesses (Hennig-Thurau et al. 2004; Yoo and Gretzel 2008), perceived self-enhancement, perceived self-image and retribution behaviors (Yoo and Gretzel 2008).

Unlike previous studies, that focus on how reviews could influence purchase decisions, or those that investigate the rationale for sharing reviews, this contribution examines the processes and motivations that lead to the articulation of exaggerated claims in testimonials (that can be either positive or negative). From the outset, this original research rejects the dominant assumption that inflated reviews are simply driven by the consumers’ egos, or from their malicious intentions. On the contrary, it suggests that altruistic appraisals that are meant to support prospective customers, constructive criticism to service providers or feedback motivated by retributive intentions, after experiencing service failures, and/or the integration of psychological self-concepts could amplify or trigger exaggerated claims in consumer reviews. As far as the authors are aware, for the time being, there are no other studies that have integrated the above factors in the same conceptual model by referring to the interpersonal deception theory as an exploratory lens. Therefore, this contribution aims to address this knowledge gap, in the tourism and hospitality industry context. The study advances a novel theoretical model that is empirically tested, in terms of the constructs’ reliabilities and validities. Moreover, it also sheds light on the significance of the causal paths that predict the consumers’ likelihood of creating exaggerated content in review platforms.

Big businesses are breaking down traditional silos among their internal departments to improve knowledge flows within their organizations and/or when they welcome external ideas and competences from external organizations (Aakhus & Bzdak, 2015; Chesbrough, 2003; Chesbrough & Bogers, 2014). Open innovation is related to the degree of trust and openness with a variety of stakeholders (Chesbrough, 2020; Leonidou et al., 2020; Zhu et al., 2019). Debately, this concept clearly differentiates itself from closed innovation approaches that are associated with traditional, secretive business models that would primarily rely on the firms’ internal competences and resources. In the latter case, the companies would withhold knowledge about their generation of novel ideas, including incremental and radical innovations within their research and development (R&D) department. They would be wary of leaking information to external parties. This is in stark contract with open innovation.

Open innovation is rooted in the belief that the dissemination of knowledge and collaboration with stakeholders would lead to win-win outcomes for all parties. Chesbrough (2003) argued that companies can maximize the potential of their disruptive innovations if they work in tandem with internal as well as with external stakeholders (rather than on their own) in order to improve products and service delivery. His open innovation model suggests that corporations ought to benefit from diverse pools of knowledge that are distributed among companies, customers, suppliers, universities, research center industry consortia, and startup firms.

Chesbrough (2020) distinguished between different types of insider information that could or could not be leaked to interested parties. He cautioned that sensitive information (he referred to as the “Crown Jewels”) ought to be protected and can never be revealed to external stakeholders. Nevertheless, he argued that an organization can selectively share specific communications with a “Middle Group” comprising key customers, suppliers, and/or partners in order to forge closer relationships with them. The companies’ internal R&D departments can avail themselves from their consumers’ insights as well as from external competences, capabilities, and resources, to cocreate value to their business and to society at large.

Chesbrough (2020) went on to suggest that a company should open-up their “long tail of intellectual property to everyone.” He contended that organizations may do so to save on their patent renewal fees. During the coronavirus (COVID-19) pandemic, many businesses joined forces and adopted such an intercompany open innovation approach to mass produce medical equipment. For instance, Ford Motor Co. sent its teams of engineers to consult with counterparts at 3M and General Electric to produce respirators, ventilators, and new 3-D-printed face shields, for the benefit of healthcare employees and COVID-19 patients (Washington Post, 2020).

Corporations are increasingly collaborating with experts hailing from diverse industry sectors to innovate themselves and to search for new sources of competitive advantage (Porter & Kramer, 2011; Roszkowska-Menkes, 2018). They may usually resort to open innovation approaches when they engage with talented individuals who work on a freelance basis or for other organizations, to benefit from their support. There is scope for companies to forge fruitful relationships with external stakeholders, who may be specialized in specific fields, to help them identify trends, penetrate into new markets, to develop new products, or to diversify their business model, to establish new revenue streams for their firm (Camilleri & Bresciani, 2022; Centobelli, Cerchione, Chiaroni, et al., 2020; Su et al., 2022). These stakeholders can add value to host organizations in their planning, organization, and implementation of social and environmentally sustainable innovations (Camilleri, 2019a; Sajjad et al., 2020).

Open innovation holds great potential to create shared value opportunities for business and society (Aakhus & Bzdak, 2015; Alberti & Varon Garrido, 2017; Roszkowska-Menkes, 2018). This argumentation is closely related to the strategic approach to corporate social responsibility (CSR) and to the discourse about corporate sustainability (Camilleri, 2022a; Eweje, 2020). Previous literature confirmed that open innovation processes can have a significant effect on the companies’ triple bottom line in terms of their economic performance as well as on their social and environmental credentials (Gong et al., 2020; Grunwald et al., 2021; Mendes et al., 2021; Testa et al., 2018).

The businesses’ ongoing engagement with their valued employees may result in a boost in their intrinsic motivations, morale, job satisfaction, and low turnover levels and could increase their productivity levels (Camilleri, 2021; Chang, 2020; Kumar & Srivastava, 2020; Schmidt-Keilich & Schrader, 2019). Their collaboration with external (expert) stakeholders may lead to positive outcomes including to knowledge acquisition, operational efficiencies, cost savings, and to creating new revenue streams from the development of innovative projects, among others (Ghodbane, 2019; Huizingh, 2011). Open innovation agreements are clearly evidenced when businesses forge strong relationships with internal and external stakeholders to help them plan, develop, promote, and distribute products (Bresciani, 2017; Camilleri, 2019b; Chesbrough & Bogers, 2014; Greco et al., 2022; Loučanová et al., 2022; Troise et al., 2021). They may do so to be in a better position to align corporate objectives (including to increase their bottom lines) with their social and environmental performance (Alberti & Varon Garrido, 2017; Herrera & de las Heras-Rosas, 2020; Mendes et al., 2021).

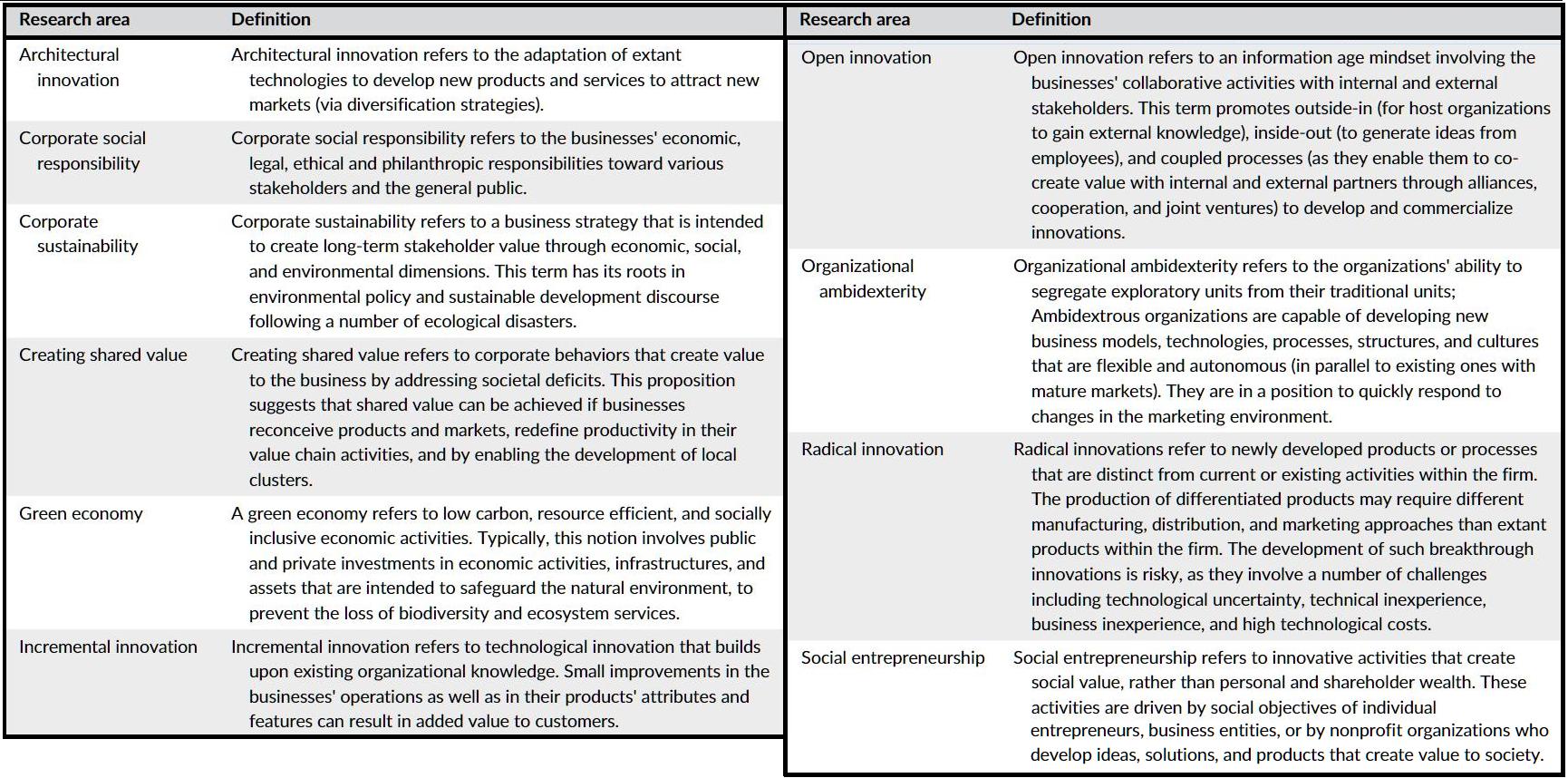

This paper provides a clear definition of the most popular paradigms relating to the intersection of open innovation approaches and corporate sustainability, as reported in Table 1.

Table 1. A list of the most popular paradigms relating to the intersection of open innovation approaches and corporate sustainability

“The following section synthesizes the content that was reported in past contributions. The researchers deliberate about open innovation opportunities and challenges for host organizations as well as for their collaborators”.

Open innovation opportunities

In the main, many commentators noted that open innovation approaches have brought positive outcomes for host organizations and their collaborators. The research questions of the extracted contributions (that are reported in Table 2) indicated that in many cases, companies are striving in their endeavors to build productive relationships with different stakeholders (Mtapuri et al., 2022; Peña-Miranda et al., 2022; Shaikh & Randhawa, 2022), to create value to their businesses as well as to society (Döll et al., 2022; Ghodbane, 2019; Roszkowska-Menkes, 2018). Very often, they confirmed that open innovation practitioners are promoting organizational governance (Aakhus & Bzdak, 2015; Sánchez-Teba et al., 2021), fair labor practices (Chang, 2020; Herrera & de las Heras-Rosas, 2020; Kumar & Srivastava, 2020; Schmidt-Keilich & Schrader, 2019), environmentally responsible investments (Aakhus & Bzdak, 2015; Cigir, 2018; Mendes et al., 2021; van Lieshout et al., 2021; Yang & Roh, 2019), and consumer-related issues (Greco et al., 2022; Loučanová et al., 2022; Wu & Zhu, 2021; Yang & Roh, 2019), among other laudable behaviors.

Many researchers raised awareness on the corporate sustainability paradigm (van Marrewijk, 2003) as they reported about the businesses’ value creating activities that are synonymous with the triple bottom line discourse, in terms of their organizations’ social, environment, and economic performance (Chang, 2020; Döll et al., 2022; Su et al., 2022; van Lieshout et al., 2021; Yang & Roh, 2019).

Other authors identified strategic CSR (Fontana, 2017; Porter & Kramer, 2006) practices and discussed about shared value perspectives (Abdulkader et al., 2020; Porter & Kramer, 2011) that are intended to improve corporate financial performance while enhancing their social and environmental responsibility credentials among stakeholders (Ghodbane, 2019; Roszkowska-Menkes, 2018; Sánchez-Teba et al., 2021).

Mendes et al. (2021) argued that strategic CSR was evidenced through collaborative approaches involving employees and external stakeholders. They maintained that there is scope for businesses to reconceive their communication designs with a wide array of stakeholders. Similarly, Aakhus and Bzdak (2015) contended that stakeholder engagement and open innovation processes led to improved decision making, particularly when host organizations consider investing in resources and infrastructures to be in a better position to address the social, cultural, and environmental concerns.

Firms could implement open innovation approaches to benefit from outsiders’ capabilities and competences (of other organizations, including funders, partners, and beneficiaries, among others) (Alberti & Varon Garrido, 2017). They may benefit from the external stakeholders’ support to diversify their business and/or to develop innovative products and services. Their involvement could help them augment their financial performance in terms of their margins and return on assets (Ben Hassen & Talbi, 2022).

Ongoing investments in open and technological innovations in terms of process and product development can result in virtuous circles and positive multiplier effects for the businesses as well as to society. Practitioners can forge cooperative agreements with social entrepreneurs, for-profit organizations, or with non-profit entities. Many companies are increasingly recruiting consultants who are specialized in sustainable innovations. Alternatively, they engage corporate reporting experts to help them improve their ESG credentials with stakeholders (Holmes & Smart, 2009).

Such open innovation approaches are intrinsically related to key theoretical underpinnings related to CSR including the stakeholder theory, institutional theory, signaling theory, and to the legitimacy theory, among others (Authors; Freudenreich et al., 2020). Firms have a responsibility to bear toward societies where they operate their business (in addition to their economic responsibility to increase profits). Their collaborative stance with knowledgeable professionals may provide an essential impetus for them to improve their corporate reputation and image with customers and prospects.

The open innovation paradigm suggests that it is in the businesses’ interest to engage with stakeholders through outside-in (to benefit from external knowledge and expertise), inside-out (to avail themselves of their extant competences and capabilities), and coupled (cocreation) processes with internal and external stakeholders (Enkel et al., 2009; Roszkowska-Menkes, 2018). Its theorists claim that outside-in processes are intended to enhance the company’s knowledge as they source external information from marketplace stakeholders including suppliers, intermediaries, customers, and even competitors, among others.

Many researchers emphasize that there are a number of benefits resulting from coopetition among cooperative competitors. Their inside-out collaborative processes stimulate innovations, lead to improvements in extant technologies, and provide complementary resources, resulting in new markets and products. Competing businesses can exchange their ideas and innovations with trustworthy stakeholders, outside of their organizations’ boundaries in order to improve their socio-emotional wealth (Herrera & de las Heras-Rosas, 2020). The proponents of open innovation advocate that businesses ought to foster an organizational culture that promotes knowledge transfer, ongoing innovations, and internationalization strategies.

Michelino et al. (2019) held that organizations ought to engage in ambidextrous approaches. These authors commended that practitioners should distinguish between exploratory and traditional units of their business model. They posited that it would be better for them if they segregated the former from the latter ones, especially if they want to develop new processes, products, and technologies in mature markets. The organizations’ exploratory units could be in a better position to flexibly respond to ongoing changes in their marketing environment.

Other researchers noted that it would be better if the businesses’ R&D activities are attuned with the practitioners’ expertise and/or with their stakeholders who are involved in their open innovation knowledge sharing strategies (Talab et al., 2018). Companies can generate new sources of revenue streams, even in areas that are associated with social issues and/or with green economies, if they reach new customers in different markets (Centobelli, Cerchione, & Esposito, 2020; Chang, 2020; Su et al., 2022; Yang & Roh, 2019). They may partner with other organizations to commercialize their (incremental or radical) innovations through licensing fees, franchises, joint ventures, mergers and acquisitions, spinoffs, and so forth.

Many commentators made reference to coupled processes involving a combination of outside-in and inside-out open innovation processes (Roszkowska-Menkes, 2018). The businesses’ transversal alliances involving horizontal and vertical collaborative approaches with external stakeholders can help them co-create ideas to foster innovations (Greco et al., 2022; Rupo et al., 2018). Several open innovation theorists are increasingly raising awareness on how collaborative relationships with stakeholders including consumers, lead users, organizations who may or may not be related to the company per se, universities as well as research institutions, among others, are supporting various businesses in their R&D stages and/or in the design of products (Khan et al., 2022; Naruetharadhol et al., 2022). Very often, their research confirmed that such cocreation processes are utilized in different contexts, for the manufacturing of a wide range of technologies.

The findings from this review reported that, for the time being, just a few researchers are integrating open innovation’s cocreation approaches with corporate sustainability outcomes. A number of contributing authors insisted that there are many advantages for socially and environmentally responsible companies to embrace open innovation approaches (Carayannis et al., 2021; Cigir, 2018; Mendes et al., 2021; Yang & Roh, 2019). In many cases, they argued that the practitioners’ intentions are to broaden their search activities and to avail themselves from talented employees and external experts in exchange for enhanced social legitimacy, thereby availing themselves of innovation capital for future enterprising activities (Greco et al., 2022; Holmes & Smart, 2009).

Hence, businesses may benefit from the competences and capabilities of individual consultants and organizations (from outside their company) to tap into the power of co-creation, to source ideas for social and green innovations (van Lieshout et al., 2021). These alliances are meant to support laudable causes, address the deficits in society, and/or to minimize the businesses’ impact on the natural environment (Altuna et al., 2015; Khan et al., 2022). For-profit organizations can resort to open innovation approaches to avail themselves of resources and infrastructures that are not currently available within their firm. This way they can reduce their costs, risks, and timescales when diversifying into sustainable business ventures, including those related to social entrepreneurship projects (Peredo & McLean, 2006; Shapovalov et al., 2019). They may do so to leverage their business, to gain a competitive advantage over their rivals.

Open innovation challenges

Open innovations could expose the businesses to significant risks and uncertainties associated with enmeshed, permeable relationships with potential collaborators (Gomes et al., 2021; Madanaguli et al., 2023). Various authors contended that practitioners should create an organizational culture that is conducive to open innovation (Herrera & de las Heras-Rosas, 2020; Mohelska & Sokolova, 2017). Generally, they argued that host organizations should communicate and liaise with employees as well as with external partners, during the generation of ideas and in different stages of their R&D projects. Some researchers noted that open innovation practitioners tend to rely on their external stakeholders’ valuable support to diversify their business models, products, or services (Chalvatzis et al., 2019; Park & Tangpong, 2021; Su et al., 2022).

A number of academic commentators argued that practitioners have to set clear, specific, measurable, attainable, relevant, and timely goals to them before they even start working on a project together (Alberti & Varon Garrido, 2017). In many cases, they maintained that host organizations are expected to foster a strong relationship with collaborators. At the same time, they should ensure that the latter ones comply with their modus operandi (Dahlander & Wallin, 2020). In reality, it may prove difficult for the business leaders to trust the new partners. Unlike their employees, the external parties are not subject to the companies’ codes of conduct, rules, and regulations (Chesbrough, 2020; Shamah & Elssawabi, 2015). A few authors indicated that senior management may utilize extrinsic and intrinsic incentives to empower and motivate internal as well as external stakeholders to pursue their organization’s open innovation objectives (Chang, 2020; Greco et al., 2022; Holmes & Smart, 2009; Roszkowska-Menkes, 2018; Schmidt-Keilich & Schrader, 2019).

Some researchers identified possible threats during and after the implementation of joint projects. Very often, they contended that host organizations risk losing their locus of control to external stakeholders who are experts in their respective fields (Madanaguli et al., 2023). The latter ones may possess unique skills and competences that are not readily available within the organization. A few authors cautioned that the practitioners as well as their collaborators are entrusted to safeguard each other’s intangible assets. A number of researchers warned and cautioned that they may risk revealing insider information about sensitive commercial details relating to their intellectual capital (Gomes et al., 2021). As a result, companies may decide to collaborate on a few peripheral tasks as they may be wary of losing their return on investments if they share trade secrets with their new partners, who could easily become their competitors. Their proprietary knowledge concerns are of course real and vital for their future prospects. Therefore, their relationships with internal and external stakeholders should be based on mutual trust and understanding in order to increase the confidence in the projects’ outcomes (Ferraris et al., 2020; Sánchez-Teba et al., 2021).

CONCLUSIONS

The companies’ ongoing engagement with internal and external stakeholders as well as their strategic CSR initiatives and environmentally sustainable innovations can generate economic value, in the long run. This review confirms that for-profit organizations are increasingly using open innovation approaches. At the same time, they are following ethical practices, adopting responsible human resources management policies, and investing in green technologies to gain institutional legitimacy and to create competitive advantages for their business. Many authors reported that their corporate sustainability behaviors can enhance their organizations’ reputation and image among customers as well as with marketplace stakeholders. At the same time, their laudable practices may even improve their corporate financial performance.

During COVID-19, many businesses turned to open innovation’s collaborative approaches. Various stakeholders joined forces and worked with other organizations, including with competitors, on social projects that benefit the communities where they operate their companies. In many cases, practitioners have realized that such partnerships with certain stakeholders (like researchers, knowledgeable experts, creative businesses, and non-governmental institutions, among others) enable their organizations to find new ways to solve pressing problems and at the same time helped them build a positive reputation. Indeed, open innovation approaches can serve as a foundation for future win-win alliances, in line with sociological research demonstrating that trust develops when partners voluntarily go the extra mile, to create value to their business and to society at large.

Yet, this research revealed that there is still a gap in the academic literature that links CSR/corporate sustainability with open collaborative approaches. At the time of writing, this paper, there were only 45 contributions on the intersection of these notions.

Suggested citation: Camilleri, M.A. & Bresciani, S. (2022). Crowdfunding small businesses and startups: A systematic review, an appraisal of theoretical insights and future research directions, European Journal of Innovation Management, https://doi.org/10.1108/EJIM-02-2022-0060

Crowdfunding is an alternative method of raising funds that is independent from financial institutions. Individual entrepreneurs, startups and established businesses can utilize online crowdfunding platforms like Indigogo, SeedInvest and GoFundMe, among others, to access finance for new ventures or existing projects, from a large number of investors, in return for products or equity stakes.

Project initiators would usually specify their financing goals and set time frames with deadlines, for their crowdfunding campaigns. If the pre-set funding goal is not met, they will not be in a position to garner any funds for their project.

The fund-raising campaigns have to appeal to as many investors as possible. Hence, initiators ought to feature engaging content, including texts, images, photos, videos, and the like, to lure investors to support their innovative ideas, startups or business ventures. They launch fundraising campaigns through various crowdfunding platforms, in different markets, to connect with online users, thereby circumventing traditional financial institutions like banks, venture capitalists and business angels.

Therefore, the crowdfunding websites curate the offerings they receive and disintermediate traditional distribution channels by connecting online users directly with project initiators.

The crowd-investors would usually put their money in those projects in which they believe will hold lucrative potential. They may be considered as shareholders if they provide capital finance, and contribute to the development and growth of crowdfunded projects.

Prospective investors might be willing to be involved in the development and success of entrepreneurial projects including startups. They may be seeking a return on investment for their monetary contributions, particularly if they believe that project initiators could deliver exceptional service quality and/or are in a position to develop new technological innovations and cutting-edge products. Hence, they will usually trust and have faith in the investees’ knowledge and capabilities to foster positive change in business and society.

The following sections critically appraise two sides of the same coin. The researchers elaborate on (i) the demand for crowdfunding products, and on (ii) the supply of crowdfunding finance.

The use of crowdfunding platforms to raise capital requirements

Small businesses and startups experience difficulties in raising modest amounts of capital. External threats from the marketing environment including the state of the economy, government regulations, tax laws, labor legislation and fluctuations in interest rates, among other issues, could have devastating effects on such entities.

As a result, they may find themselves in an equity gap, if they cannot raise finance to foster innovation for their business. Their access to equity or debt financing through traditional institutions like banks and/or other financial service providers is usually very limited. Typically, they are required to provide a collateral to obtain finance, even though, young enterprises and startups with promising opportunities for potential investment may usually prefer having a lower debt/equity ratio.

In the past decade, a number of individuals, groups, organizations as well as entrepreneurs and startups resorted to crowdfunding, to finance their ideas, ventures or projects. The most popular crowdfunding products include donation-based crowdfunding, rewards-based crowdfunding, equity crowdfunding, peer-to-peer (P2P) lending/lending crowdfunding, and debt-securities crowdfunding, among others.

⚫The peer-to-peer lending is very similar to traditional borrowing from a bank as crowd investors lend money to a company with the understanding that they will be repaid with interest.

⚫Equity crowdfunding projects may usually involve the sale of a stake of a business to a number of investors. This type of crowdfunding is very similar to venture capital finance.

⚫Investors may be drawn to rewards-based crowdfunding to receive non-financial rewards, such as goods or services, in exchange of their contributions.

⚫Alternatively, individuals may be willing to donate their funds for charitable, humanitarian or philanthropic purposes, without expecting any financial returns

Project initiators of successful crowdfunding campaigns are capable of communicating their business propositions and solutions, as they raise awareness on disruptive innovations among large audiences through digital media.

The diffusion of innovations theory suggests that there are five key elements that could influence the diffusion of a new idea (through crowdfunding platforms), including the innovation itself, adopters/users, communication/media channels, time, as well as social systems. Crowdfunding platforms allow creators to promote their projects to generate interest and to ultimately lure investors. Notwithstanding, project initiators as well as the crowdfunding investors are affected by various communication channels, including by competing organizations and regulatory institutions.

The subjective norms in society can influence the individuals’ intentions to use innovations like crowdfunding platforms. The crowdfunding projects could attract the attention of competitors, who may be quicker to develop technological innovations or substitute products, as they could have access to financial capital, economies of scale and scope, to mimic small businesses and start-ups’ ideas.

Debatably, this argumentation is synonymous with the resource-based view theory (RBV). New businesses like startups, as well as small businesses may usually possess fewer resources including liquidity, than established businesses. They may also have access to limited competences and capabilities. Notwithstanding, they may not be considered as legitimate as their larger counterparts by their stakeholders, including by the government, creditors, venture capitalists and other investors.

However, in the past decade, a number of regulatory institutions have introduced legislation in various contexts (like the U.S.’s Jumpstart Our Business Startups – JOBS Act). These laws and the revisions that followed, were intended to support early-stage companies and startups to raise their financial requirements through crowdfunding avenues.

Crowdfunding allows for the democratization of funding, as it is essentially borderless and not geographically constrained. Businesses, enterprises and startups can use crowdfunding platforms to raise funds for on their projects. They can appeal to larger audiences through the digital media.

Project initiators are encouraged to engage with online investors through crowdfunding platforms, to provide feedback relating to products or services, in order to increase their chances of reaching their financial goals. Ultimately, it is in their interest to disseminate relevant content to project backers for transparency purposes, and to improve their credentials with stakeholders.

Investments in crowd funding products

Generally, crowdfunding links the creators/proponents of projects with potential investors. The latter ones could avail of crowdfunding digital platforms to reduce their search and transaction costs. These online users hope to identify lucrative investment opportunities that could yield them attractive returns. Such investors may be drawn by high-quality, market-oriented (commercial) projects and by their rewards, as opposed to community-oriented, not-for-profit projects with social or environmental purposes, that may be promoted via low minimum prices, to appeal to sponsors.

Project initiators of commercial entities may be wary of providing details of their intellectual properties (particularly during the early stages of their crowdfunding campaigns), as they may be concerned that someone could steal their ideas, innovations and projects. They could (willingly or unwillingly) decide not to disclose material information like historic defaults or hidden costs, even after the investor becomes a member of the crowdfunding platform.

As a result, investors of crowdfunded projects may not always have adequate and sufficient information on the borrowers of finance, as crowdfunding platforms may not exercise thorough due diligence on their users. This argument is related to the reasoning behind the signaling theory. In fact, many researchers relied on this theory to explore the signals that are communicated by project creators to lure investments from crowd funders.

Notwithstanding, the most popular crowdfunding platforms may or may not operate from the same jurisdiction of the crowd-investors. Hence, they are not always offering complete protection according to local legislation and regulations. Thus, they could not guarantee the same level of comprehensive appraisals that are provided by local financial service providers. This contentious issue could lead to problems related to information asymmetry. In some circumstances, the failure to disclose material information to crowd-investors may result in near-fraudulent consequences.

Investors may usually try to find a tradeoff between potential rewards and risks from crowdfunding opportunities. They could be attracted by (higher than normal) potential returns that certain crowd-funding activities claim to offer. Therefore, they ought to be cautious and vigilant on their possible risks of default.

If equity crowdfunded projects fail, investors could not be in a position to pay back capitals and to provide any returns to their investors. Similarly, the investors of P2P crowdfunding/lending may also risk losing their funds through unsecured loans, especially if the borrowers did not require any collateral. The investors of equity financing may encounter certain difficulties, other than default. They can find out that there is no lucrative secondary market for their shares. As a result, they might find themselves liquidating them at a significant loss, or of diluting their stock value.

Conclusions

This contribution discusses about the benefits and costs of using crowdfunding platforms to raise finance, or as plausible investment options. The authors elaborate about various challenges and identify opportunities for project initiators (like small business and startups), as well as for crowd-investors.

Currently, there are just a few articles that are linking this timely topic with key theoretical underpinnings relating to technology adoption and/or innovation management (e.g. Diffusion of Innovations Theory, Technology Acceptance Model (TAM), Theory of Planned Behavior (TPB), Theory of Reasoned Action (TRA) or the Unified Theory of Acceptance and Use of Technology (UTAUT), strategic management (e.g. Decision-making Theory; Goal Attainment Theory or RBV), accounting and financial reporting (E.g. Signaling Theory or Venture Quality Theory), and normative/business ethics research (e.g. Social Capital Theory, Social Responsibility Theory and Stakeholder Theory), among others.

For the time being, there are limited discursive contributions on crowdfunding of small businesses and startups. This research sought to address this gap in the academic literature. It clearly outlines the facilitators and barriers of using crowdfunding platforms for crowd sourcing and/or for crowd investing purposes, to better understand the demand / supply for crowdfunding.

In future, other researchers may explore the crowd sourcing possibilities of different types of businesses including sole proprietorships, partnerships, limited partnerships, limited liability companies (LLCs), nonprofits, and cooperatives (co-ops), among other entities. They may categorize enterprises, according to their staff count. Prospective authors could investigate the financing of micro enterprises, small and medium sized enterprises (SMEs), intermediate-sized enterprises and/or large-sized enterprises. Moreover, they could even distinguish among various start-ups like small business startups, scalable startups, buyable startups and/or off-shoot startups, et cetera.

This is an excerpt from my latest open-access researchthat was accepted for publication in Sustainability (IF: 2.576)

Citation: Camilleri, M.A. (2021). The Employees’ State of Mind during COVID-19: A Self-Determination Theory Perspective. Sustainability, 13, 3634. https://doi.org/10.3390/su13073634

Academic Implications

This empirical research has presented a critical review of the self-determination theory and its key constructs, as well as on other theoretical underpinnings that were drawn from business ethics and tourism literature. It shed light on the employees’ job security as well as on their extrinsic and intrinsic motivations in their workplace environment. Moreover, it explored their perceptions on their employers’ CSR practices during COVID-19. The study hypothesized that the employees’ identified motivations, introjected motivations, external motivations, job security and their firms’ socially responsible behaviors would have a positive and significant effect on their intrinsic motivations and organizational performance. The findings confirmed that the employees’ intrinsic motivations were predicting their productivity. This relationship was highly significant. Evidently, the employees were satisfied in their job, as they fulfilled their self-determination and intrinsic needs for competence, autonomy and relatedness [15,48,56]. Their high morale in their workplace environment has led to positive behavioral outcomes, including increased organizational performance.

The results reported that there were highly significant effects between the employees’ identified motivations and intrinsic motivations, and between their perceptions on their firms’ socially responsible practices and their intrinsic motivations. The mediation analysis indicated that these two constructs were indirectly affecting the employees’ job performance. These results suggest that although previous studies reported that extrinsic factors could undermine the intrinsic motivations of individuals [35–37], this study found that the research participants have internalized and identified themselves with their employers’ extrinsically motivated regulations, as they enabled them to achieve their self-defining goals. In this case, the respondents indicated that they were willing to perform certain tasks, as they perceived that their utilitarian values were also sustaining their psychological well-being and self-evaluations. The employees also identified motivations that led as an incentive to increase their organizational performance. The empirical results have proved that the employees were motivated to work for firms that reflected their own values [60,77]. This research is consistent with other contributions on CSR behaviors [32,78,88,90,91]. The respondents suggested that their employers had high CSR credentials. The findings revealed that the businesses’ CSR practices enhanced their employees’ intrinsic motivations and satisfied their psychological needs of belongingness and relatedness. Evidently, the firms’ socially responsible behaviors were enhancing their employees’ productivity and performance in their workplace environment.

The participants’ beliefs about their job security were also found to be a significant antecedent of their intrinsic motivations. Their perceptions on their job security were affecting their morale at work, in a positive manner [22,61]. During COVID-19, many employees could have experienced reduced business activities. As a result, many businesses could have pressurized their employees in their organizational restructuring and/or by implementing revised conditions of employment, including reduced working times, changes in sick leave policies, et cetera, particularly during the first wave of the pandemic. However, despite these contingent issues, the research participants indicated that they perceived that there will be job continuity for them in the foreseeable future. This study indicated that many employees were optimistic about their job prospects during the second wave.

The findings suggest that employees are attracted by and motivated to work for trustworthy, socially responsible employers [43,62,66,75]. On the other hand, they reported that the participants’ introjected and external motivations were not having a significant effect on their intrinsic motivations and did not entice them to engage in productive behaviors during the COVID-19 crisis. A plausible justification for this result is that the participants were well aware that their employers did not have adequate and sufficient resources during COVID-19. Their employers were not in a position to reward or incentivize their employees due to financial constraints that resulted from their reduced business activities or were never prepared to deal with such an unprecedented contingent situation. Hence, external motivations were not considered as stable forms of regulation [36]. Many researchers noted that extrinsic motivations will not necessarily influence the individuals’ behaviors, as their perceived locus of control is external to them. Therefore, their actions will not be autonomous and self-determined [35,52].

Managerial Implications Businesses are continuously affected by ongoing challenges arising from their macro environment. The pandemic has exacerbated their transformation on behavioral, cultural and organizational levels. The first wave of COVID-19 was devastating for many businesses, in different contexts. The social-distancing procedures have led to changes in their working conditions and diminished communications. Many of the non-essential businesses were expected to follow their government’s preventative measures to slow the spread of the pandemic and to close the doors to their customers. Moreover, several employees have experienced their employers’ cost cutting exercises, as they reduced salaries and wages. These uncertainties have affected their employees’ psychological capital and caused them anxiety and frustration [99]. Notwithstanding, many employees were concerned about their job security and long-term prospects. During the work-from-home scenario, employers had to finds new ways to manage their employees’ performance. The change in their working environment allowed them to do their work, whilst also attending to personal needs. Very often, employees found themselves taking other responsibilities including parenting/schooling their children.

Remote working has served as a reminder to managers that there are a number of non-work-related factors that can affect their employees’ mindsets and engagement levels. Hence, many employers set virtual meetings with their human resources to inject a sense of purpose in them. During the first wave of the pandemic, the employees’ intrinsic motivations have declined with the decreasing visibility of their management or colleagues. The lack of motivation could have led to a decrease in their productivity levels [3]. Therefore, employers were expected to look after their employees and to foster a culture of trust and recognition to improve their motivations and performance at work [64]. This study was carried out during the second wave, when many governments had eased their preventative restrictions to restart their economy. As a result, many employees were returning to work. They were encouraged to work in a new normal, where they were instructed to follow their employers’ health and safety policies as well as hygienic and sanitizing practices in their premises. They introduced hygienic practices, temperature checks and expected visitors to wear masks to reduce the spread of the virus.

Many businesses, including SMEs and startups, were benefiting of their governments’ financial assistance. Resources were allocated to support them in their cashflow requirements, to minimize layoffs and to secure the employment of many employees. These measures instilled confidence in employers, as they provided their employees with a sense of relatedness, competence and autonomy in their workplace environments. Evidently, employers were successful in fostering a cohesive culture where they identified their employees’ values and their self-determined goals [45]. In sum, this contribution revealed that employees felt a sense of belonging in their workplace environment. The results confirmed that their intrinsic motivations were enhancing their productivity levels and organizational performance.

References (This section presents all the references that were featured in the full paper)

Han, E.; Tan, M.M.J.; Turk, E.; Sridhar, D.; Leung, G.M.; Shibuya, K.; Asgari, N.; Oh, J.; García-Basteiro, A.L.; Hanefeld, J.; et al. Lessons learnt from easing COVID-19 restrictions: An analysis of countries and regions in Asia Pacific and Europe. Lancet 2020, 396, 1525–1534. [CrossRef]

He, H.; Harris, L. The Impact of Covid-19 Pandemic on Corporate Social Responsibility and Marketing Philosophy. J. Bus. Res. [CrossRef]

An, M.A.; Han, S.L. Effects of experiential motivation and customer engagement on customer value creation: Analysis of psychological process in the experience-based retail environment. J. Bus. Res. 2020, 120, 389–397. [CrossRef]

Van den Broeck, A.; Ferris, D.L.; Chang, C.H.; Rosen, C.C. A review of self-determination theory’s basic psychological needs at work. J. Manag. 2016, 42, 1195–1229. [CrossRef]

Vansteenkiste, M.; Simons, J.; Lens, W.; Sheldon, K.M.; Deci, E.L. Motivating learning, performance, and persistence: The synergistic effects of intrinsic goal contents and autonomy-supportive contexts. J. Pers. Soc. Psychol. 2004, 87, 246–260. [CrossRef]

Deci, E.L.; Ryan, R.M. The “what” and “why” of goal pursuits: Human needs and the self-determination of behavior. Psychol. Inq. 2000, 11, 227–268. [CrossRef]

Mitchell, R.; Schuster, L.; Jin, H.S. Gamification and the impact of extrinsic motivation on needs satisfaction: Making work fun? J.Bus. Res. 2020, 106, 323–330. [CrossRef]

Vansteenkiste, M.; Neyrinck, B.; Niemiec, C.P.; Soenens, B.; De Witte, H.; Van den Broeck, A. On the relations among work value orientations, psychological need satisfaction and job outcomes: A self-determination theory approach. J. Occup. Org. Psychol. 2007, 80, 251–277. [CrossRef]

Gagné, M.; Deci, E.L. Self-determination theory and work motivation. J. Org. Behav. 2005, 26, 331–362. [CrossRef]

Leroy, H.; Anseel, F.; Gardner, W.L.; Sels, L. Authentic leadership, authentic followership, basic need satisfaction, and work role performance: A cross-level study. J. Manag. 2015, 41, 1677–1697. [CrossRef]

Vansteenkiste, M.; Ryan, R.M. On psychological growth and vulnerability: Basic psychological need satisfaction and need frustration as a unifying principle. J. Psychother. Integr. 2013, 23, 263. [CrossRef]

Berezan, O.; Krishen, A.S.; Agarwal, S.; Kachroo, P. Exploring loneliness and social networking: Recipes for hedonic well-being on Facebook. J. Bus. Res. 2020, 115, 258–265. [CrossRef]

Raub, S.; Robert, C. Differential effects of empowering leadership on in-role and extra-role employee behaviors: Exploring the role of psychological empowerment and power values. Hum. Relat. 2010, 63, 1743–1770. [CrossRef]

Guo, Y.; Liao, J.; Liao, S.; Zhang, Y. The mediating role of intrinsic motivation on the relationship between developmental feedback and employee job performance. Soc. Behav. Pers. Int. J. 2014, 42, 731–741. [CrossRef]

Quinn, R.W.; Spreitzer, G.M.; Lam, C.F. Building a sustainable model of human energy in organizations: Exploring the critical role of resources. Acad. Manag. Ann. 2012, 6, 337–396. [CrossRef]

Mahmoud, A.B.; Reisel, W.D.; Fuxman, L.; Mohr, I. A motivational standpoint of job insecurity effects on organizational citizenship behaviors: A generational study. Scand. J. Psychol. 2020. [CrossRef]

Baard, P.P.; Deci, E.L.; Ryan, R.M. Intrinsic need satisfaction: A motivational basis of performance and well-being in two work settings. J. App. Soc. Psychol. 2004, 34, 2045–2068. [CrossRef]

Ajzen, I. The theory of planned behavior. Org. Behav. Hum. Dec. Proc. 1991, 50, 179–211. [CrossRef]

Moon, T.W.; Hur, W.M.; Hyun, S.S. How service employees’ work motivations lead to job performance: The role of service employees’ job creativity and customer orientation. Curr. Psychol. 2019, 38, 517–532. [CrossRef]

Deci, E.L.; Olafsen, A.H.; Ryan, R.M. Self-determination theory in work organizations: The state of a science. Ann. Rev. Org. Psychol. Org. Behav. 2017, 4, 19–43. [CrossRef]

Chang, J.H.; Teng, C.C. Intrinsic or extrinsic motivations for hospitality employees’ creativity: The moderating role of organizationlevel regulatory focus. Int. J. Hosp. Manag. 2017, 60, 133–141. [CrossRef]

Wang, W.T.; Hou, Y.P. Motivations of employees’ knowledge sharing behaviors: A self-determination perspective. Inf. Org. 2015, 25, 1–26. [CrossRef]

Hau, Y.S.; Kim, B.; Lee, H.; Kim, Y.G. The effects of individual motivations and social capital on employees’ tacit and explicit knowledge sharing intentions. Int. J. Inf. Manag. 2013, 33, 356–366. [CrossRef]

Ryan, R.M.; Deci, E.L. Self-determination theory and the facilitation of intrinsic motivation, social development, and well-being. Amer. Psychol. 2000, 55, 68–79. [CrossRef]

Amabile, T.M. Motivational synergy: Toward new conceptualizations of intrinsic and extrinsic motivation in the workplace. Hum. Res. Manag. Rev. 1993, 3, 185–201. [CrossRef]

Asante Boadi, E.; He, Z.; Bosompem, J.; Opata, C.N.; Boadi, E.K. Employees’ perception of corporate social responsibility (CSR) and its effects on internal outcomes. Serv. Ind. J. 2020, 40, 611–632. [CrossRef]

Diamantidis, A.D.; Chatzoglou, P. Factors affecting employee performance: An empirical approach. Int. J. Prod. Perf. Manag. 2019, 68, 171–193. [CrossRef]

Millette, V.; Gagné, M. Designing volunteers’ tasks to maximize motivation, satisfaction and performance: The impact of job characteristics on volunteer engagement. Motiv. Emot. 2008, 32, 11–22. [CrossRef]

Zhang, J.; Zhang, Y.; Song, Y.; Gong, Z. The different relations of extrinsic, introjected, identified regulation and intrinsic motivation on employees’ performance: Empirical studies following self-determination theory. Manag. Dec. 2016, 54, 2393–2412. [CrossRef]

Li, Y.; Sheldon, K.M.; Liu, R. Dialectical thinking moderates the effect of extrinsic motivation on intrinsic motivation. Learn. Individ. Differ. 2015, 39, 89–95. [CrossRef]

Nijhof, A.H.J.; Jeurissen, R.J.M. The glass ceiling of corporate social responsibility: Consequences of a business case approach towards CSR. Int. J. Soc. Soc. Policy 2010, 30, 618–631. [CrossRef]

Kuvaas, B.; Dysvik, A. Perceived investment in employee development, intrinsic motivation and work performance. Hum. Res. Manag. J. 2009, 19, 217–236. [CrossRef]

Yakhlef, A.; Nordin, F. Effects of firm presence in customer-owned touch points: A self-determination perspective. J. Bus. Res. [CrossRef]

Ryan, R.M. Control and information in the intrapersonal sphere: An extension of cognitive evaluation theory. J. Pers. Soc. Psychol. 1982, 43, 450–461. [CrossRef]

Allison, T.H.; Davis, B.C.; Short, J.C.; Webb, J.W. Crowdfunding in a prosocial microlending environment: Examining the role of intrinsic versus extrinsic cues. Entrep. Theory Pr. 2015, 39, 53–73. [CrossRef]

Malik, M.A.R.; Butt, A.N.; Choi, J.N. Rewards and employee creative performance: Moderating effects of creative self-efficacy, reward importance, and locus of control. J. Organ. Behav. 2015, 36, 59–74. [CrossRef]

Buil, I.; Catalán, S.; Martínez, E. Understanding applicants’ reactions to gamified recruitment. J. Bus. Res. 2020, 110, 41–50. [CrossRef]

Gomez-Baya, D.; Lucia-Casademunt, A.M. A self-determination theory approach to health and well-being in the workplace: Results from the sixth European working conditions survey in Spain. J. Appl. Soc. Psychol. 2018, 48, 269–283. [CrossRef]

Wallace, J.C.; Butts, M.M.; Johnson, P.D.; Stevens, F.G.; Smith, M.B. A multilevel model of employee innovation: Understanding the effects of regulatory focus, thriving, and employee involvement climate. J. Manag. 2016, 42, 982–1004. [CrossRef]

Dicke, T.; Marsh, H.W.; Parker, P.D.; Guo, J.; Riley, P.; Waldeyer, J. Job satisfaction of teachers and their principals in relation to climate and student achievement. J. Educ. Psychol. 2020, 112, 1061–1073. [CrossRef]

Harris, K.; Hinds, L.; Manansingh, S.; Rubino, M.; Morote, E.S. What Type of Leadership in Higher Education Promotes Job Satisfaction and Increases Retention? J. Leadership Instr. 2016, 15, 27–32.

Kovjanic, S.; Schuh, S.C.; Jonas, K.; Quaquebeke, N.V.; Van Dick, R. How do transformational leaders foster positive employee outcomes? A self-determination-based analysis of employees’ needs as mediating links. J. Org. Behav. 2012, 33, 1031–1052. [CrossRef] Sustainability 2021, 13, 3634 16 of 17

Lemos, M.S.; Veríssimo, L. The relationships between intrinsic motivation, extrinsic motivation, and achievement, along elementary school. Proc. Soc. Behav. Sci. 2014, 112, 930–938. [CrossRef]

Deci, E.L.; Ryan, R.M. The general causality orientations scale: Self-determination in personality. J. Res. Pers. 1985, 19, 109–134. [CrossRef]

Lee, S.; Pounders, K.R. Intrinsic versus extrinsic goals: The role of self-construal in understanding consumer response to goal framing in social marketing. J. Bus. Res. 2019, 94, 99–112. [CrossRef]

Burton, K.D.; Lydon, J.E.; D’Alessandro, D.U.; Koestner, R. The differential effects of intrinsic and identified motivation on well-being and performance: Prospective, experimental, and implicit approaches to self-determination theory. J. Pers. Soc. Psychol. 2006, 91, 750–762. [CrossRef]

Wolf, T.; Weiger, W.H.; Hammerschmidt, M. Experiences that matter? The motivational experiences and business outcomes of gamified services. J. Bus. Res. 2020, 106, 353–364. [CrossRef]

Gagné, M.; Forest, J.; Gilbert, M.H.; Aubé, C.; Morin, E.; Malorni, A. The motivation at work scale: Validation evidence in two languages. Educ. Psychol. Meas. 2010, 70, 628–646. [CrossRef]

Greguras, G.J.; Diefendorff, J.M. Different fits satisfy different needs: Linking person-environment fit to employee commitment and performance using self-determination theory. J. Appl. Psychol. 2009, 94, 465–477. [CrossRef] [PubMed]

Giri, V.N.; Kumar, B.P. Assessing the impact of organizational communication on job satisfaction and job performance. Psychol. Stud. 2010, 55, 137–143. [CrossRef]

Grant, A.M. Does intrinsic motivation fuel the prosocial fire? Motivational synergy in predicting persistence, performance, and productivity. J. Appl. Psychol. 2008, 93, 48–58. [CrossRef] [PubMed]

Meyer, J.P.; Stanley, L.J.; Parfyonova, N.M. Employee commitment in context: The nature and implication of commitment profiles. J. Vocat. Behav. 2012, 80, 1–16. [CrossRef]

Kraimer, M.L.; Wayne, S.J.; Liden, R.C.; Sparrowe, R.T. The role of job security in understanding the relationship between employees’ perceptions of temporary workers and employees’ performance. J. Appl. Psychol. 2005, 90, 389–398. [CrossRef]

Loi, R.; Ngo, H.Y.; Zhang, L.; Lau, V.P. The interaction between leader–member exchange and perceived job security in predicting employee altruism and work performance. J. Occup. Org. Psychol. 2011, 84, 669–685. [CrossRef]

Cheng, G.H.L.; Chan, D.K.S. Who suffers more from job insecurity? A meta-analytic review. Appl. Psychol. 2008, 57, 272–303. [CrossRef]

Yidong, T.; Xinxin, L. How ethical leadership influence employees’ innovative work behavior: A perspective of intrinsic motivation. J. Bus. Eth. 2013, 116, 441–455. [CrossRef]

Sverke, M.; Hellgren, J.; Näswall, K. No security: A meta-analysis and review of job insecurity and its consequences. J. Occup. Health Psychol. 2002, 7, 242–264. [CrossRef]

Shin, Y.; Hur, W.M.; Moon, T.W.; Lee, S. A motivational perspective on job insecurity: Relationships between job insecurity, intrinsic motivation, and performance and behavioral outcomes. Int. J. Environ. Res. Pub. Health 2019, 16, 1812. [CrossRef] [PubMed]

Brammer, S.; Millington, A.; Rayton, B. The contribution of corporate social responsibility to organizational commitment. Int. J. Hum. Res. Manag. 2007, 18, 1701–1719. [CrossRef]

Drucker, P.F. Converting social problems into business opportunities: The new meaning of corporate social responsibility. Calif. Manag. Rev. 1984, 26, 53–63. [CrossRef]

Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [CrossRef]

Windsor, D. Corporate social responsibility: Three key approaches. J. Manag. Stud. 2006, 43, 93–114. [CrossRef]

Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 1991, 34, 39–48. [CrossRef]

Hao, Y.; Farooq, Q.; Zhang, Y. Unattended social wants and corporate social responsibility of leading firms: Relationship of intrinsic motivation of volunteering in proposed welfare programs and employee attributes. Corp. Soc. Resp. Environ. Manag. 2018, 25, 1029–1038. [CrossRef]

Ashforth, B.E.; Mael, F. Social identity theory and the organization. Acad. Manag. Rev. 1989, 14, 20–39. [CrossRef]

Tajfel, H. Social identity and intergroup behaviour. Soc. Sci. Inf. 1974, 13, 65–93. [CrossRef]

Hur, W.M.; Moon, T.W.; Ko, S.H. How employees’ perceptions of CSR increase employee creativity: Mediating mechanisms of compassion at work and intrinsic motivation. J. Bus. Eth. 2018, 153, 629–644. [CrossRef]

Skudiene, V.; Auruskeviciene, V. The contribution of corporate social responsibility to internal employee motivation. Balt. J. Manag. 2012, 7, 49–67. [CrossRef]

Vlachos, P.A.; Panagopoulos, N.G.; Rapp, A.A. Feeling good by doing good: Employee CSR-induced attributions, job satisfaction, and the role of charismatic leadership. J. Bus. Eth. 2013, 118, 577–588. [CrossRef]

Valentine, S.; Fleischman, G. Ethics programs, perceived corporate social responsibility and job satisfaction. J. Bus. Eth. 2008, 77, 159–172. [CrossRef]

Archimi, C.S.; Reynaud, E.; Yasin, H.M.; Bhatti, Z.A. How perceived corporate social responsibility affects employee cynicism: The mediating role of organizational trust. J. Bus. Eth. 2018, 151, 907–921. [CrossRef]

Hansen, S.D.; Dunford, B.B.; Boss, A.D.; Boss, R.W.; Angermeier, I. Corporate social responsibility and the benefits of employee trust: A cross-disciplinary perspective. J. Bus. Eth. 2011, 102, 29–45. [CrossRef]

Kim, J.S.; Milliman, J.; Lucas, A. Effects of CSR on employee retention via identification and quality-of-work-life. Int. J. Cont. Hosp. Manag. 2020, 32, 1163–1179. [CrossRef]

Lee, L.; Chen, L.F. Boosting employee retention through CSR: A configurational analysis. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 948–960. [CrossRef]

Zhu, Q.; Yin, H.; Liu, J.; Lai, K.H. How is employee perception of organizational efforts in corporate social responsibility related to their satisfaction and loyalty towards developing harmonious society in Chinese enterprises? Corp. Soc. Responsib. Environ. Manag. 2014, 21, 28–40. [CrossRef]

Lee, E.M.; Park, S.Y.; Lee, H.J. Employee perception of CSR activities: Its antecedents and consequences. J. Bus. Res. 2013, 66, 1716–1724. [CrossRef]

Petrenko, O.V.; Aime, F.; Ridge, J.; Hill, A. Corporate social responsibility or CEO narcissism? CSR motivations and organizational performance. Strat. Manag. J. 2016, 37, 262–279. [CrossRef]

Camilleri, M.A. Measuring the corporate managers’ attitudes toward ISO’s social responsibility standard. Total Qual. Manag. Bus. Excel. 2019, 30, 1549–1561. [CrossRef]

Nazir, O.; Islam, J.U. Influence of CSR-specific activities on work engagement and employees’ innovative work behaviour: An empirical investigation. Curr. Issues Tour. 2020, 23, 3054–3072. [CrossRef]

Gond, J.P.; El Akremi, A.; Swaen, V.; Babu, N. The psychological microfoundations of corporate social responsibility: A personcentric systematic review. J. Org. Behav. 2017, 38, 225–246. [CrossRef]

MacKenzie, S.B.; Podsakoff, P.M. Common method bias in marketing: Causes, mechanisms, and procedural remedies. J. Retail. 2012, 88, 542–555. [CrossRef]

Deal, J.J.; Stawiski, S.; Graves, L.; Gentry, W.A.; Weber, T.J.; Ruderman, M. Motivation at work: Which matters more, generation or managerial level? Consult. Psychol. J. Pr. Res. 2013, 65, 1–16. [CrossRef]

Camilleri, M.A. The promotion of responsible tourism management through digital media. Tour. Plan. Dev. 2018, 15, 653–671. [CrossRef]

Singh, J.; Del Bosque, I.R. Understanding corporate social responsibility and product perceptions in consumer markets: A cross-cultural evaluation. J. Bus. Eth. 2008, 80, 597–611. [CrossRef]

Hair, J.F.; Sarstedt, M.; Ringle, C.M.; Mena, J.A. An assessment of the use of partial least squares structural equation modeling in marketing research. J. Acad. Mark. Sci. 2012, 40, 414–433. [CrossRef]

Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [CrossRef]

Mao, Y.; He, J.; Morrison, A.M.; Andres Coca-Stefaniak, J. Effects of tourism CSR on employee psychological capital in the COVID-19 crisis: From the perspective of conservation of resources theory. Curr. Issues Tour. 2020, 1–19. [CrossRef]

This authoritative book features a broad spectrum of theoretical and empirical contributions on topics relating to corporate communications in the digital age. It is a premier reference source and a valuable teaching resource for course instructors of advanced, undergraduate and post graduate courses in marketing and communications. It comprises fourteen engaging and timely chapters that appeal to today’s academic researchers including doctoral candidates, postdoctoral researchers, early career academics, as well as seasoned researchers. All chapters include an abstract, an introduction, the main body with headings and subheadings, conclusions and research implications. They were written in a critical and discursive manner to entice the curiosity of their readers.